Mastering Secondary Market Transactions: A Strategic Guide for Modern Enterprises

- Jamille Cummins

- May 21

- 12 min read

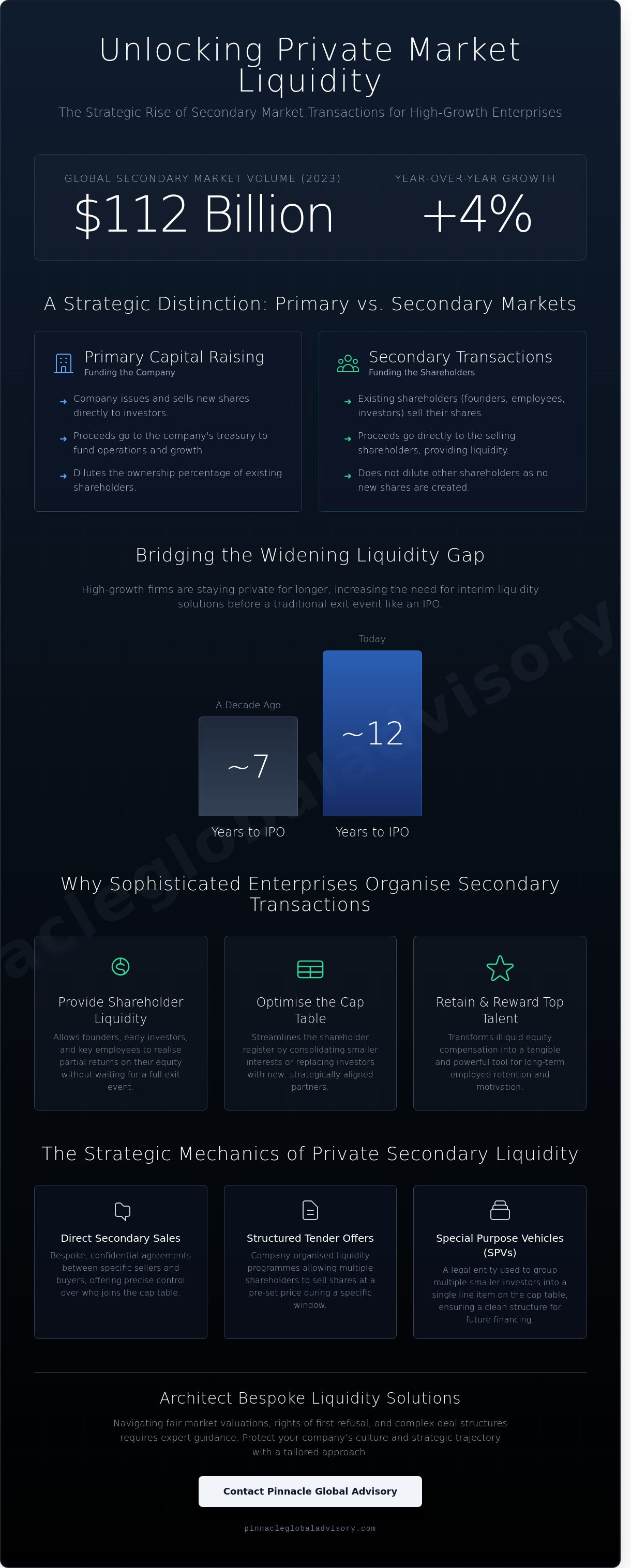

What if the traditional path to liquidity is no longer the most efficient route to your firm's next summit? Whilst many leaders believe that value remains trapped until a full exit event occurs, the rise of secondary market transactions has fundamentally altered the trajectory for private enterprises. In 2023, global secondary market volume reached an estimated $112 billion, representing a 4% increase from the previous year. You likely recognise the frustration of managing locked-up equity whilst your long-term stakeholders wait for a distant horizon.

It's understandable to feel that misaligned shareholder timelines and the complexity of valuing private shares create unnecessary friction in your strategic planning. This guide will demonstrate how a bespoke approach to these transactions provides the vital liquidity and strategic flexibility your organisation requires to thrive. We'll explore how to achieve partial liquidity, clean up your cap table, and reward the talent driving your success without the pressure of a premature exit.

Key Takeaways

Understand how secondary market transactions distinguish themselves from primary capital raising by prioritising liquidity for existing shareholders whilst maintaining a clean cap table.

Explore the strategic use of Special Purpose Vehicles and structured tender offers to consolidate interests and streamline your corporate structure for future growth.

Discover how to bridge the "liquidity gap" for founders and key staff, transforming equity into a powerful tool for long-term talent retention and alignment.

Learn the essential steps for establishing fair market valuations and navigating complex rights of first refusal to ensure a seamless and compliant execution.

Realise the transformative impact of expert global guidance in architecting bespoke liquidity solutions that protect your company's unique culture and strategic trajectory.

Defining Secondary Market Transactions in a Modern Corporate Landscape

In the sophisticated architecture of global finance, secondary market transactions represent the vital pulse of liquidity that sustains an organisation's long-term health. Unlike the initial issuance of shares, these transactions involve the exchange of existing securities amongst investors, ensuring that capital remains fluid even as it remains committed to a company’s growth trajectory. By the start of 2026, the strategic landscape has shifted significantly; high-growth enterprises are opting to remain private for longer, often delaying initial public offerings by an average of 12 years compared to the seven-year cycles observed a decade ago. This shift has elevated the secondary market from a niche alternative to a cornerstone of Global Strategic capital management.

While public exchanges like the London Stock Exchange (LSE) offer a highly visible arena for these trades, the private sphere requires a more nuanced approach. We see this as mastering the terrain between immediate liquidity needs and the preservation of a company’s cap table integrity. It’s about ensuring that as an enterprise ascends toward its strategic summit, the transition of ownership remains seamless and aligned with the overarching vision. Precision in these matters is non-negotiable.

Primary vs. Secondary: A Strategic Distinction

The distinction between these two markets is fundamental to any Global capability. Primary markets serve to fund the company itself, providing the dry powder necessary for expansion; secondary markets, conversely, fund the shareholders. This dual-track system creates a balanced corporate ecosystem where early backers can realise gains without disrupting the company’s operational excellence. Crucially, secondary market transactions don't typically dilute existing shareholders, as no new shares are minted. Instead, they facilitate a transfer of value that maintains the equilibrium of the existing equity structure. It's a mechanism for stability.

The Evolution of the Private Secondary Market

The methodology surrounding private liquidity has matured from sporadic, one-off sales into sophisticated, company-led liquidity programmes. In the current climate, elite advisory firms manage these processes to ensure every trade supports the broader Global trajectory of the business. This oversight prevents the fragmentation of the shareholder base and ensures that new entrants are strategically aligned with the firm's future. The aftermarket is defined as the period following a security’s initial issuance. Transitioning into this phase requires a disciplined framework where strategic foresight replaces reactive decision-making. By implementing structured windows for trade, leaders can ensure that the pursuit of liquidity never compromises the long-term stability of the firm’s mission.

The Strategic Mechanics of Private Secondary Liquidity

Achieving liquidity in the private sector requires more than just a willing buyer; it demands a sophisticated architectural approach to deal structure. These secondary market transactions serve as a vital release valve for capital, allowing stakeholders to realise value without the immediate necessity of an IPO or a full company sale. By leveraging specific formats, firms can maintain their strategic trajectory whilst satisfying the diverse needs of their cap table. It's about creating a balance between individual exit requirements and the long-term health of the business.

Direct Secondary Sales and Structured Tender Offers

Direct sales function as bespoke agreements between individual sellers and targeted buyers. These are often highly confidential, allowing for precise control over who enters the share register. However, they can be administratively taxing. In contrast, structured tender offers are company-organised events. Jefferies reported that global secondary volume reached $114 billion in 2023, a testament to how these organised windows allow multiple shareholders to exit at a pre-set price. Whilst tender offers require more upfront coordination, they offer a cleaner, more unified process that reduces long-term legal friction and keeps the executive team focused on operational excellence.

The Role of Special Purpose Vehicles (SPVs)

Maintaining a streamlined share register is essential for any business eyeing a future summit. SPVs act as a consolidation tool, allowing various smaller interests to be grouped under a single legal entity. This ensures the cap table remains organised, which is a critical factor for institutional investors during later-stage funding rounds. For those seeking a deeper technical understanding of these structures, our analysis of what is an SPV provides the necessary context. This method ensures that secondary market transactions don't result in a fragmented and unmanageable list of shareholders that could complicate future governance.

Institutional secondary funds play a pivotal role here, acting as sophisticated partners that specialise in purchasing private equity. Their presence often facilitates Management Buy-Outs (MBOs) by providing the exit capital needed for departing founders. This allows the remaining management team to take the reins without the distraction of a broader market auction. If you're looking to master the terrain of private equity exits, our global advisory team can help align your vision with execution. This strategic foresight ensures that every transition serves the long-term stability and pinnacle performance of the enterprise.

Why Sophisticated Enterprises Organise Secondary Transactions

Sophisticated leadership teams recognise that the path to a global summit is rarely a straight line. As the median age of venture-backed companies reaching an IPO stretched to 12.5 years in 2023, according to data from the University of Florida, the traditional "wait and see" approach to liquidity has become obsolete. Secondary market transactions offer a bespoke mechanism to manage this extended timeline. They ensure that the company’s internal engine remains fuelled whilst the external trajectory stays ambitious.

Solving the Liquidity Gap for Founders and Employees

A founder whose personal wealth is entirely locked within their enterprise often faces a psychological burden that can stifle bold, transformative moves. When 90% of your net worth is illiquid, the natural human desire to protect what you've built can sometimes overshadow the need to innovate aggressively. By facilitating a secondary sale, founders can de-risk their personal lives. This shift in mindset allows them to return to the boardroom with the strategic foresight required for another five or ten years of growth. It’s about creating a sense of security that fosters long-term vision rather than short-term caution.

This strategy is equally vital for the workforce. Early-stage staff members who joined a company in 2015 shouldn't have to wait until 2027 to see the tangible fruits of their labour. Providing a liquidity window acts as a powerful retention tool. It rewards excellence and ensures your most talented minds don't depart for a competitor simply because they need to realise value for a mortgage deposit or family commitments. When employees see a clear path to liquidity, their alignment with the company’s long-term success strengthens.

Re-aligning the Cap Table for Long-term Trajectory

Not every investor who backed your vision at the seed stage is equipped to support a multi-billion pound global expansion. Most venture capital funds operate on a strict 10-year lifecycle. Once that clock runs out, the pressure on the CEO to deliver an exit increase significantly, regardless of whether the company is actually ready for the public markets. Secondary market transactions allow for a graceful transition that benefits all parties. You can replace "tired" capital with institutional partners who possess longer investment horizons and deeper pockets.

Facilitates a clean exit for early angels and seed funds whose mandates have been met.

Introduces strategic partners who align with the current operational scale and future complexity.

Removes the desperate need for a premature trade sale or IPO that might undervalue the business.

This proactive management of the cap table ensures that your shareholders are as committed to the future as the executive team. It’s a process of curation, ensuring the investor base evolves alongside the company. By masterfully handling these transitions, a business avoids the friction of misaligned incentives. You aren't just moving shares; you're ensuring the entire organisation is positioned for the final ascent to industry dominance.

Navigating the Complexities of a Successful Secondary Transaction

Orchestrating secondary market transactions is a sophisticated manoeuvre that demands more than simple financial brokerage. It requires a disciplined, five-step framework to ensure the company’s trajectory remains undisturbed whilst providing liquidity to early stakeholders. This process begins with establishing a fair market valuation, followed by defining eligibility through Right of First Refusal (ROFR) constraints. Leaders must then manage the delicate flow of information to new investors and ensure rigorous regulatory compliance across global jurisdictions, such as the UK and Australia. The final summit involves executing the transfer with a level of precision that prevents operational friction.

Valuation and Pricing in an Illiquid Market

Establishing a price in the absence of a public ticker requires strategic foresight. Most boards rely on the most recent primary funding round or a formal 409A valuation as a baseline. However, secondary shares rarely trade at par with primary equity. Data from 2023 indicates that secondary interests often trade at a 20% to 30% discount compared to the most recent preferred round. This gap reflects the lack of liquidation preferences and the inherent illiquidity of the asset. Transparency amongst all participating parties is the only way to maintain the trust necessary for a bespoke deal. When pricing is handled with quiet assurance, it reinforces the brand’s stability in the eyes of Global investors.

Managing Stakeholder Alignment and Rights

The legal terrain of a secondary sale is often cluttered with transfer restrictions and board-level hurdles. The Right of First Refusal is a common barrier where the company or existing investors hold the power to match any outside offer, potentially cooling interest from new buyers. Clear communication is vital here to prevent rumours from eroding internal morale. When new institutional capital enters the cap table, the expertise of buy-side m&a advisory is indispensable. This ensures that the new entrants’ goals align perfectly with the company’s long-term vision.

Compliance adds another layer of complexity. In the UK, transactions must align with the Financial Services and Markets Act 2000. Managing these secondary market transactions requires a partner who understands these global nuances. The objective is a seamless execution that allows the C-suite to focus on operational excellence rather than administrative distractions. Precision at this stage ensures the company’s reputation remains at its pinnacle.

Secure your company's future by partnering with experts who master the art of equity transition. Consult with our Global strategic advisors today.

How Strategic Advisory Elevates Secondary Market Outcomes

Attempting to navigate secondary market transactions without expert guidance often leads to fragmented cap tables and misaligned incentives. Whilst a "do-it-yourself" approach might seem cost-effective initially, it lacks the institutional weight required to attract the right calibre of buyer. Leaders who manage these sales internally often struggle with valuation benchmarks and the complexities of shareholder rights. We believe that true liquidity shouldn't come at the expense of your company's soul. At Pinnacle Global Advisory, we act as the architects of bespoke liquidity solutions, ensuring that every share transfer respects the established culture and long-term mission of your enterprise.

Our global network isn't just a list of contacts; it's a curated ecosystem of institutional investors who value stability and vision. Identifying the right partner requires more than a simple introduction. It demands a deep understanding of how an incoming shareholder will influence the board's chemistry. By leveraging our international reach, we find buyers who aren't just looking for an entry point, but who align with your specific growth trajectory. This level of strategic matching transforms a routine sale into a hallmark of a mature, visionary business.

From Transactional Execution to Strategic Foresight

Strategic advisors look far beyond the immediate exchange of capital. We focus on how the transaction affects your company's valuation in the next funding round or exit event. According to Lazard’s 2023 Secondary Market Report, transaction volumes reached approximately $114 billion, driven by a growing need for sophisticated liquidity management. This scale requires a high level of discretion. In high-stakes corporate transitions, a leak can destabilise employee morale or alert competitors. We maintain absolute professionalism, ensuring the process remains confidential whilst achieving the "pinnacle" of strategic alignment between buyers and sellers.

Partnering with Pinnacle Global Advisory

Our firm specialises in managing the complexities that define modern corporate transitions. Whether you're facilitating Management Buy-Outs (MBOs) or seeking structured capital solutions, we provide the clarity needed to make informed decisions. We don't just provide a service; we offer a partnership that values your time and your legacy. Secondary liquidity can be a powerful tool for retention and growth when it's part of a broader, well-constructed plan. We invite you to Connect with our global advisory team to discuss your liquidity strategy and discover how we can help you master the terrain of the global markets.

Charting Your Trajectory Toward Strategic Alignment

Mastering the complex terrain of secondary market transactions requires more than just technical execution; it demands a visionary approach to corporate liquidity. As the Jefferies 2023 Global Secondary Market Review confirms, with annual volumes reaching $112 billion, these manoeuvres have become a cornerstone of sophisticated capital management. By prioritising strategic foresight, your enterprise can successfully navigate management buyouts whilst ensuring long-term stability for every stakeholder involved. It's about more than just moving assets; it's about reaching the summit of operational excellence through precise, high-level guidance.

At Pinnacle Global Advisory, we specialise in the bespoke capital solutions that high-growth enterprises require to maintain their upward momentum. Our Global network of sophisticated institutional investors and our deep expertise in complex corporate transitions provide the stability you need to scale. We're here to ensure your vision and execution remain in perfect alignment as you navigate these high-stakes transitions. Partner with Pinnacle Global Advisory to navigate your secondary market strategy and secure your position at the top of your industry. You've built an exceptional organisation; now it's time to realise its full potential on the global stage.

Frequently Asked Questions

What is the primary difference between a primary and secondary market transaction?

The core distinction lies in who receives the capital. In a primary transaction, the company issues new shares to investors and receives the proceeds to fund its Global expansion. Conversely, secondary market transactions involve the sale of existing shares between investors or employees, meaning the capital flows to the seller rather than the company's balance sheet. Jefferies reported that secondary volume reached approximately $114 billion in 2023, highlighting the scale of these liquidity events.

Can a private company block a secondary sale of its shares?

Yes, most private companies maintain strict control over their cap table through Right of First Refusal (ROFR) clauses and transfer restrictions. These legal frameworks typically grant the company 30 to 60 days to match an external offer and purchase the shares themselves. By exercising these rights, a board can ensure that equity remains within a curated circle of partners who align with the firm's long-term strategic trajectory and operational excellence.

How does a secondary transaction affect a company’s valuation?

Whilst secondary market transactions don't technically alter the official post-money valuation from a primary round, they provide vital price discovery. These trades often occur at a discount of 20% to 50% compared to the most recent Series funding. This data point helps leadership teams gauge the market's current appetite and informs the strategic foresight needed for future capital raises. It's a pragmatic look at what the market believes the summit of the company's value actually is.

Who are the typical buyers in a private secondary market transaction?

Buyers are generally sophisticated institutional investors, such as dedicated secondary funds, family offices, or venture capital firms looking to increase their stake. Specialised entities like Lexington Partners or Coller Capital manage billions in capital specifically for these bespoke opportunities. These elite partners provide the liquidity necessary for early employees and investors to realise their gains without waiting for a traditional exit, such as an IPO or a full acquisition.

Are there tax implications for employees selling shares in a secondary transaction?

Selling equity is a taxable event that usually triggers Capital Gains Tax (CGT) obligations. In the United Kingdom, for the 2024/25 tax year, the annual exempt amount is £3,000, with gains above this taxed at 10% for basic rate payers and 20% for those in higher brackets. It's essential to consult a professional advisor to navigate these complexities, as the specific structure of your shares can significantly alter the final tax burden you'll face.

Do secondary transactions cause dilution for existing shareholders?

Secondary transactions don't result in dilution because the company isn't issuing new equity. The total number of shares in the company's capital structure remains exactly the same; only the name on the share certificate changes. This stability ensures that existing shareholders maintain their exact percentage of ownership whilst allowing the seller to achieve their personal financial goals. It's a clean transfer of value that preserves the established alignment of the cap table.

What is a tender offer in the context of private secondary markets?

A tender offer is a structured, company-led event where a buyer offers to purchase shares from multiple eligible employees and investors at a fixed price. These programmes are often used by high-growth firms like SpaceX to provide periodic liquidity to their team. Under SEC Rule 14e-1, these offers must typically remain open for at least 20 business days. This organised approach ensures a fair process and allows the company to manage the entry of new strategic partners effectively.

How long does a typical private secondary transaction take to complete?

A bespoke secondary sale usually requires 60 to 90 days to reach its conclusion. This timeline accounts for the initial price negotiation, the standard 30-day ROFR notice period, and the final legal documentation required for a secure transfer. Whilst it's a more deliberate pace than public market trades, this duration allows for the thorough due diligence and board approvals necessary to maintain the integrity of a company's private standing and long-term vision.

Comments